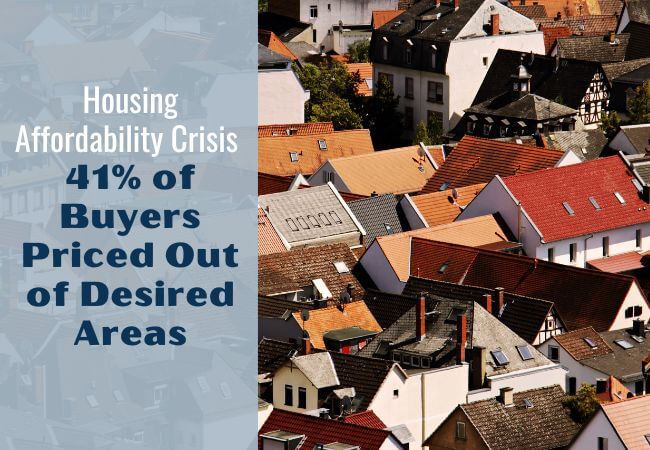

Buyers priced out

Some 41% of participants in a recent survey¹ agreed with the statement, ‘I cannot afford to live in the area I want or need to live in’. Many renters and homeowners alike were unhappy with their current location, with job opportunities (37%), proximity to friends and family (35%) and a better lifestyle (29%) as the key reasons for wanting or needing to move elsewhere.

Holiday lets bounce back

In the early weeks of 2023, 173 more mortgage options were on the market for holiday let borrowers than in October 2022², and a broad range of fixed and variable options remain available now. After the September ‘mini-budget’, the range plummeted to only 26 lenders, but investors’ appetites have picked up as ‘staycations’ remain a popular holiday choice.

Hard resell for new builds

One in eight new-build homes are being resold at a loss, figures sho³, with flats making up more than four-fifths of these loss-making sales. The average new-build property lost 7.8% (£22,000) of its value, with the typical sale taking place after 8.8 years. New builds are often sold at a premium, which can mean prices fall back to market rate when resold.

Get in touch

Clifford Osborne are Independent Financial Advisors (IFA) based in Eastbourne, East Sussex, offering mortgage advice, early retirement advice, pension advice and more get in touch for a chat with one of our friendly advisers.

We see clients across Sussex and Kent, including Eastbourne, Uckfield, Lewes, Brighton, Tunbridge Wells, Hastings, Bexhill, Newhaven, Seaford, Crowborough and further afield.

Why not read our VoucherFor reviews to see what our clients have to say?

¹kindroom, 2023, ²Moneyfacts, 2023, ³Hamptons, 2023

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments

It is important to take professional advice before making any decision relating to your personal finances. Information within this blog is based on our current understanding of taxation and can be subject to change in future.

It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK; please ask for details. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

If you withdraw from an investment in the early years, you may not get back the full amount you invested. Changes in the rates of exchange may have an adverse effect on the value or price of an investment in sterling terms if it is denominated in a foreign currency. Taxation depends on individual circumstances as well as tax law and HMRC practice which can change.

The information contained within the blog is for information purposes only and does not constitute financial advice.

The purpose of the blog is to provide technical and general guidance and should not be interpreted as a personal recommendation or advice.